Financial needs are constantly piling up faster than anticipated, in today’s Kenyan economy. Whether the needs are for education, medical expenses, or starting a business, access to quick and convenient loans becomes essential.

In Kenya, one popular option is unsecured debt. This blog post aims to provide a comprehensive guide to unsecured debt, covering everything from the institutions that offer it, the application process, advantages, potential risks, and more.

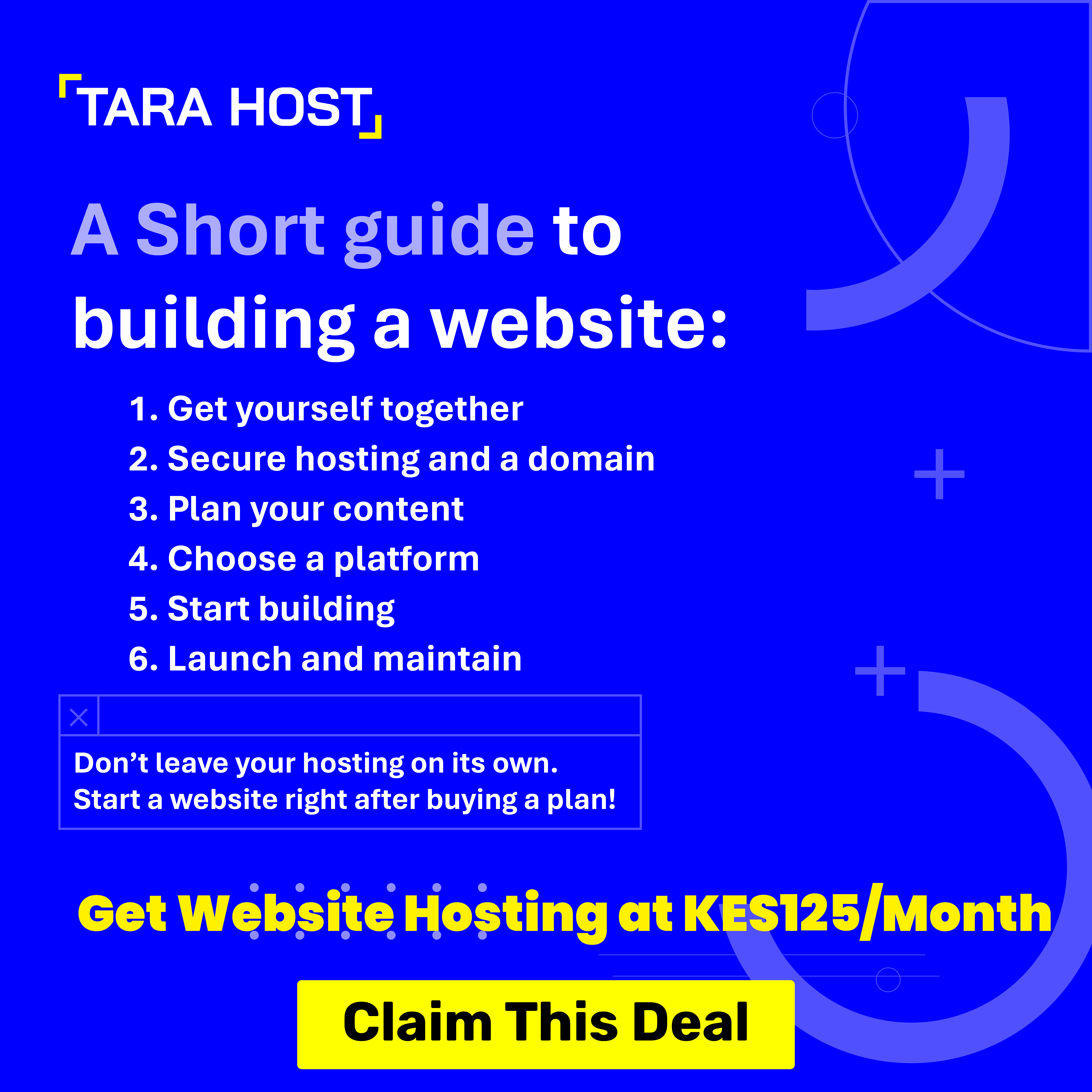

Keep focus…

Where can you get unsecured debt in Kenya?

Several institutions in Kenya provide unsecured debt to individuals in need. These institutions are as follows:

- Banks – Commercial banks like Equity Bank, Standard Chartered Bank, and Kenya Commercial Bank (KCB) offer unsecured personal loans to qualified applicants.

- Microfinance Institutions (MFIs) – These include entities such as Faulu Kenya, KWFT, and Musoni Microfinance provide unsecured loans specifically tailored to meet the financial requirements of individuals who may not meet the strict criteria set by traditional banks.

- Digital Lenders – In recent years, digital lending platforms such as Tala, Branch, Okasg, Branch, Creditmoja etc., have gained popularity in Kenya. These platforms use innovative technology to assess creditworthiness and provide unsecured loans conveniently through mobile applications.

How Can You Apply for Unsecured Debt in Kenya?

Here is a generalized procedure on how to apply for an unsecured loan in Kenya;

- Research: Begin by researching different institutions that offer unsecured loans. Compare interest rates, repayment terms, and eligibility criteria to find the best fit for your needs.

- Gather Required Documents: Prepare necessary documents such as identification (ID card, passport), proof of income, bank statements, and any other supporting documents requested by the lending institution.

- Application: Visit the chosen institution’s website or branch to complete the loan application. Digital lenders often provide an application process within their mobile apps.

- Credit Assessment: The lending institution will assess your creditworthiness by evaluating your credit history, income, and other relevant factors. This process may involve a credit check.

- Loan Approval and Disbursement: If your application is approved, you will receive an offer detailing the loan amount, interest rate, and repayment terms. Upon acceptance, the funds will be disbursed to your bank account or mobile wallet.

Advantages of Unsecured Debt

- Quick Access: Unsecured loans are typically processed faster than secured loans, providing quick access to much-needed funds in times of urgency.

- No Collateral Requirement: Unlike secured loans that require collateral, unsecured debt doesn’t put your assets at risk. This is particularly beneficial for individuals who do not possess significant assets or prefer not to pledge them.

- Flexible Use: Unsecured loans can be used for various purposes, such as debt consolidation, education expenses, medical emergencies, home renovations, or starting a small business. The flexibility allows borrowers to meet their specific financial needs.

- Improved Credit History: Timely repayment of unsecured loans can positively impact your credit history, potentially improving your credit score over time.

Common Questions That People Frequently Ask

What is the maximum loan amount I can get through unsecured debt in Kenya?

The maximum loan amount varies depending on the lending institution and the borrower’s creditworthiness. Generally, it ranges from Ksh 500 to Ksh 5,000,000.

Are unsecured loans available for self-employed individuals in Kenya?

Yes, many institutions offer unsecured loans to self-employed individuals, provided they can demonstrate a stable income source and meet other eligibility criteria.

Risks Associated with Unsecured Debt

- Higher Interest Rates: Unsecured loans often come with higher interest rates compared to secured loans. Borrowers should carefully consider the interest rates and ensure they can comfortably manage the loan repayments.

- Risk of Default: Since unsecured loans do not require collateral, lenders face a higher risk of non-repayment. Defaulting on loan payments can lead to severe consequences, including damage to credit history and legal action by the lender.

- Potential Debt Cycle: The ease of obtaining unsecured loans can sometimes lead individuals into a cycle of borrowing, resulting in a debt burden that becomes difficult to manage. Borrowers should exercise caution and borrow only what they can afford to repay.

Conclusion

Unsecured debt provides a valuable financial solution for individuals in Kenya who require quick access to funds without the need for collateral.

Institutions such as banks, microfinance institutions, and digital lenders offer unsecured loans with varying terms and conditions. However, borrowers should carefully evaluate the advantages and risks associated with unsecured debt before making borrowing decisions. By understanding the application process, assessing their own financial capabilities, and considering alternative options, individuals can make informed decisions to meet their financial needs responsibly.